Why most software startups don't need VCs anymore (most)

AI collapsed development costs by 90%. The VC model wasn't built for this.

A year ago, ambitious software startups budgeted $500,000 for AI API costs. Today, the same workload costs $50,000, and the output is better.

This 90% cost collapse isn't just a pricing story. It's the beginning of the end for venture capital in software.

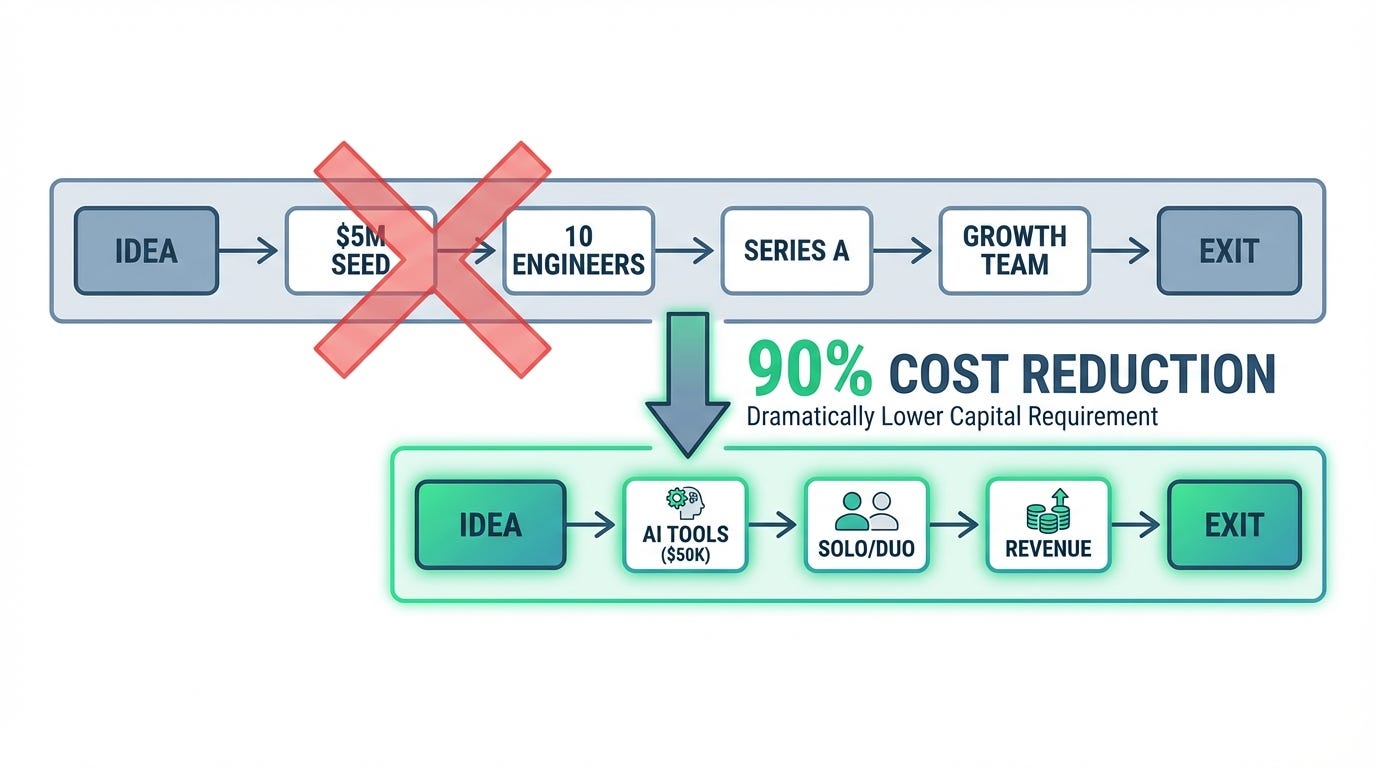

The VC model was built for a world where shipping software required large teams and significant capital. Hire 10 engineers, pay Bay Area salaries, burn cash until product-market fit, raise more, repeat. That model made sense when software was expensive to build.

But AI changed the math. When a solo founder can bootstrap a company with $10-20K and sell it for $80 million six months later, something fundamental has shifted. The question isn't whether VCs will adapt. It's whether they're still necessary for most software startups.

They're not.

The old model: Why software startups needed VCs

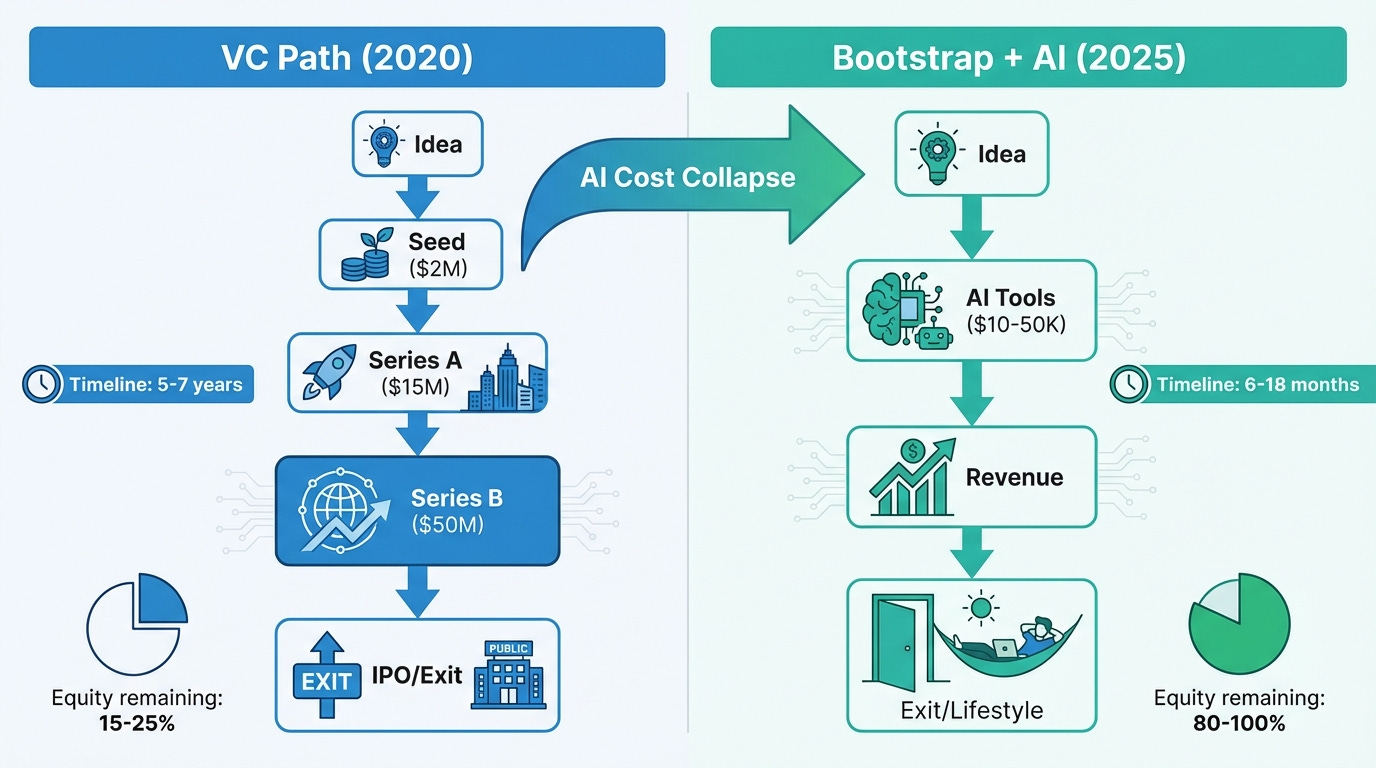

The economics of a pre-AI software startup were brutal. Engineers in San Francisco cost $200K+ fully loaded. You needed a team of 5-10 to ship anything meaningful. Add designers, product managers, DevOps. Factor in 18-24 months to reach product-market fit. The math was simple: building software required millions of dollars.

VCs solved this problem. They provided the capital to hire fast, ship faster, and outrun competitors who were also burning cash. The implicit bargain was clear: founders gave up 20-30% of their company in exchange for the runway to scale a team.

Speed was the product VCs were really selling. Capital bought speed. Speed bought market share. Market share justified the next round at a higher valuation. The flywheel depended on high burn rates, because high burn rates meant you were deploying capital effectively.

This logic worked when software was labor-intensive. It assumed that the primary constraint on shipping was having enough engineers.

The new math: What AI actually changed

That constraint is gone.

OpenAI's token costs fell 90% in a single year. The market for AI coding tools hit $4 billion in 2025, up 4x year-over-year, representing 55% of all departmental AI spending. Half of all developers now use AI coding tools daily, and in high-performing organizations, that number hits 65%.

These aren't incremental improvements. They represent a structural shift in how software gets made.

The efficiency gains are concrete: 30-40% reduction in operational costs, 40-70% faster delivery cycles. One founder put it this way: "I can build full websites, backend apps, and workflows in one or a few days, not weeks. I don't need a team of five. Just a few smart tools and a git repo."

To be clear: AI tools don't eliminate the work of shipping production-grade software. Security audits, observability, scalability, and compliance still require human judgment. But they do compress the time-to-MVP dramatically. What took three months now takes three weeks. What required five engineers now requires one.

The proof point is Base44, though it comes with a caveat. Maor Shlomo, who previously co-founded Explorium (which raised $130 million), started Base44 as a side project in late 2024. His prior exit gave him domain expertise, a network, and credibility that first-time founders lack. But the economics of what he achieved are still instructive: He bootstrapped it with around $10-20K of his own money, used Cursor as his dev environment, and made the company profitable as a one-person operation. By May 2025, Base44 was generating $189K in monthly profit. In June, Wix acquired it for approximately $80 million.

No seed round. No Series A. No cap table full of VCs. Just AI tools and a solo founder who knew how to use them.

The mismatch: VCs need to deploy, startups don't need to accept

The venture capital industry has a structural problem: funds are sized for a different era.

VCs raise large funds, often $500 million or more. They need to deploy that capital across dozens of companies. Writing $500K checks doesn't move the needle on fund returns. The model pushes toward larger rounds: $5 million seeds, $20 million Series A, $50 million Series B.

But if AI has reduced the capital requirements for building software by 70-80%, those round sizes are now absurd for most software startups. A $5 million seed is five years of runway for a two-person team using AI tools. It's far more than most founders need to reach profitability or a meaningful exit.

The math does depend on your market. If you're building dev tools with product-led growth, AI-powered bootstrapping is viable. If you're selling to enterprises with 12-month sales cycles, you still need capital for sales teams and customer acquisition. The $5 million seed isn't absurd for enterprise software; it's absurd for the growing category of tools that can reach profitability before needing to hire.

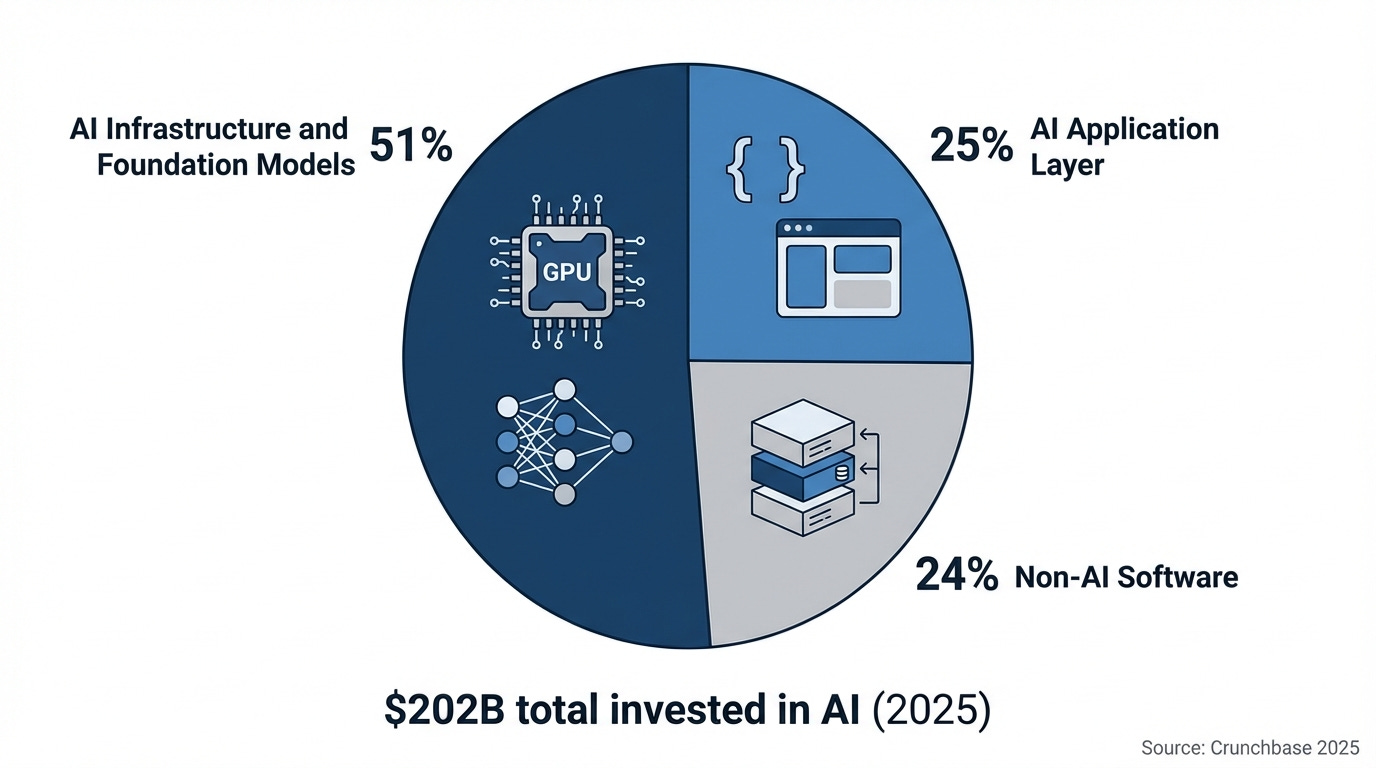

VCs have responded rationally: they're chasing the companies that still need massive capital. According to Crunchbase, AI captured 51% of all global VC dollars in 2025, up from 37% in 2024 and 26% in 2023. The $202 billion invested in AI represented a 75% year-over-year increase. Foundation model companies like OpenAI, Anthropic, xAI, and Mistral commanded the largest checks.

This concentration makes sense. Training frontier AI models costs hundreds of millions, sometimes billions. Building GPU clusters requires real capital. The VC model still works for capital-intensive AI infrastructure.

But it leaves traditional software starved. The bifurcation is stark: AI startups receive premium valuations (42% higher at seed stage) while non-AI software companies struggle to attract interest. VCs are shifting capital away from non-AI plays entirely.

What VCs still buy (and where they still matter)

Venture capital isn't dying everywhere. It's becoming hyperspecialized.

VCs remain essential for genuinely capital-intensive businesses. AI infrastructure (training clusters, data centers, foundation models), hardware, and robotics still require the kind of upfront investment that justifies giving up equity. Anthropic being valued at $183 billion makes sense when training runs cost tens of millions of dollars.

VCs also buy go-to-market scale. Enterprise software with long sales cycles, geographic expansion, and brand-building marketing campaigns can benefit from VC-level capital. If your product requires a 50-person sales team to win deals, VC money accelerates that.

Regulatory moats are another justification. Fintech, healthcare, and legal tech startups often face compliance costs that dwarf development costs. Building a licensed bank or navigating FDA approvals requires capital that exceeds what AI can compress.

And winner-take-all markets can still justify VC economics. When being first to scale determines the entire market outcome, speed matters more than capital efficiency. The question is whether that describes most software markets. It doesn't.

The new path: What replaces VC-funded software startups?

The alternative is already emerging.

The percentage of startups launched by solo founders without VC rose from 22% in 2015 to 38% in 2024. The practical tooling to support this shift is mature: Cursor for development, Lovable for landing pages, Claude Code for code generation, all usable by founders without deep technical backgrounds.

Revenue-based financing has grown as an alternative to equity dilution. When your startup costs $50K to build instead of $5M, taking on debt or revenue-share agreements makes more sense than giving up 20% of your company.

The exit paths are changing too. Acqui-hires used to be consolation prizes. Now they're the plan. Base44's $80 million acquisition wasn't a pivot from a failed fundraise. It was a bootstrapped company reaching a successful exit without ever needing outside capital.

Team structures reflect the new economics. Stack Overflow's 2025 survey shows 76% of developers now use or plan to use AI coding tools. AI isn't just making individual developers more productive. It's making small teams viable for projects that previously required large organizations.

The one-person unicorn is the logical endpoint of AI-assisted development. Not a fantasy, an inevitability. Base44 reached $80 million in value; the first solo founder to hit $1 billion is a matter of when, not if.

What happens to VCs?

The venture capital industry will consolidate.

Fewer funds will survive. Those that do will concentrate on capital-intensive AI infrastructure, hardware, and genuinely scale-dependent markets. The seed stage for software will shrink dramatically. Writing small checks to software startups won't generate returns when those startups don't need to raise subsequent rounds.

This is already visible in the data. Deal counts for AI-related investments declined 13% year-over-year in 2025, even as dollar values surged. Capital is concentrating at the top. The broad-based AI FOMO of 2023-2024 has given way to disciplined bets on a smaller number of foundation-level companies.

Many investors privately expect overvaluations from 2025 to face pressure in 2026 as ROI demands increase. The tuck-in acquisitions, acqui-hires, and wind-downs are coming for startups that raised at inflated prices but can't justify continued investment.

For VCs, the uncomfortable truth is that the model was built for a different era. When software required labor, capital bought labor. When software requires AI tools, capital buys... what, exactly? A subscription to Cursor? The marginal value of a $5 million check has collapsed along with the cost of development.

The recommendation

Before you pitch your next seed round, do the math.

Can you reach profitability or a meaningful milestone with $50K instead of $5M? Can you build with a team of two instead of twenty? If the answer is yes, you don't need VC money. You certainly don't need to give up 25% of your company for capital you won't deploy.

For VCs reading this: the concentration in AI infrastructure is the rational response. But don't pretend the software seed stage is coming back. It's not. The economics have shifted permanently.

The VC model assumed that startups needed to buy engineers' time. AI changed that equation. You can now rent intelligence by the token, and the price is dropping faster than venture returns can justify.

VCs used to buy your ability to hire. Now AI is the new hire. And it doesn't need a recruiter.